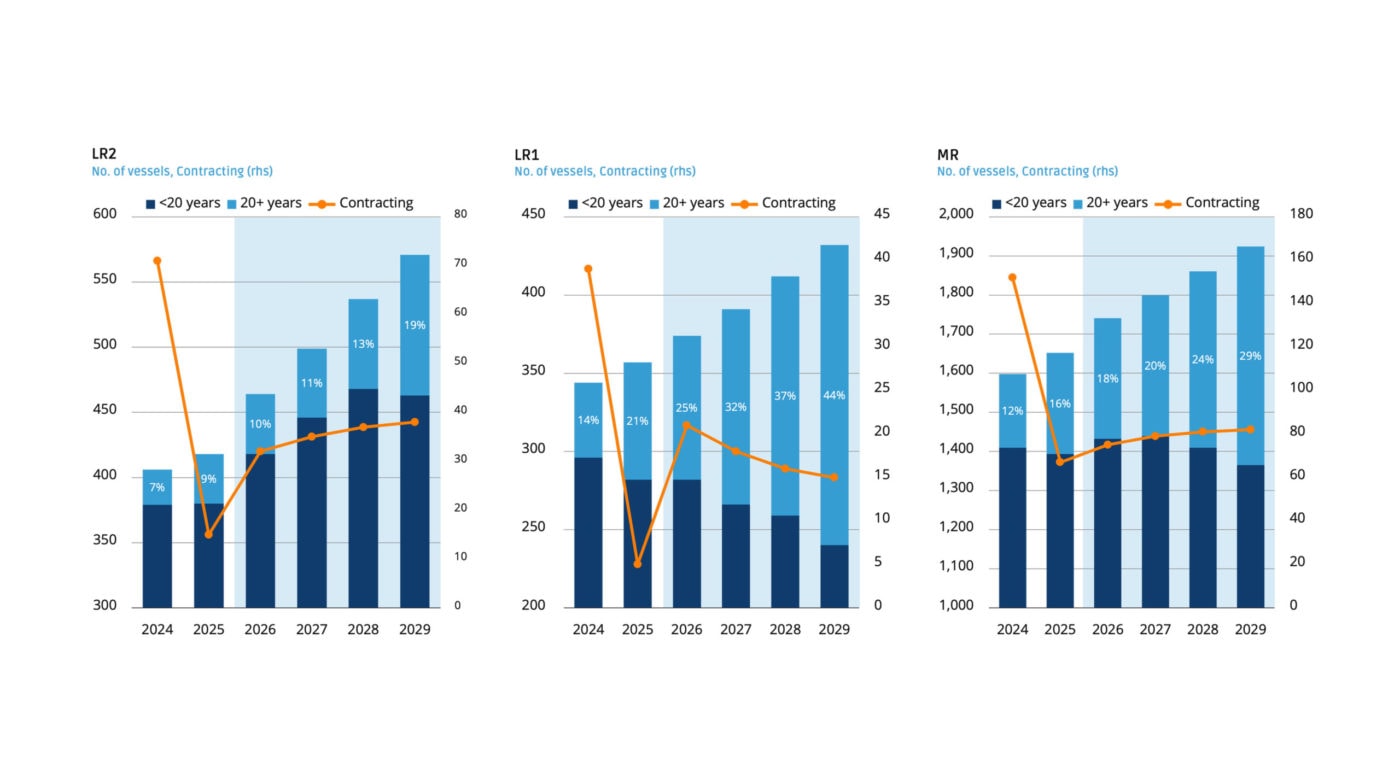

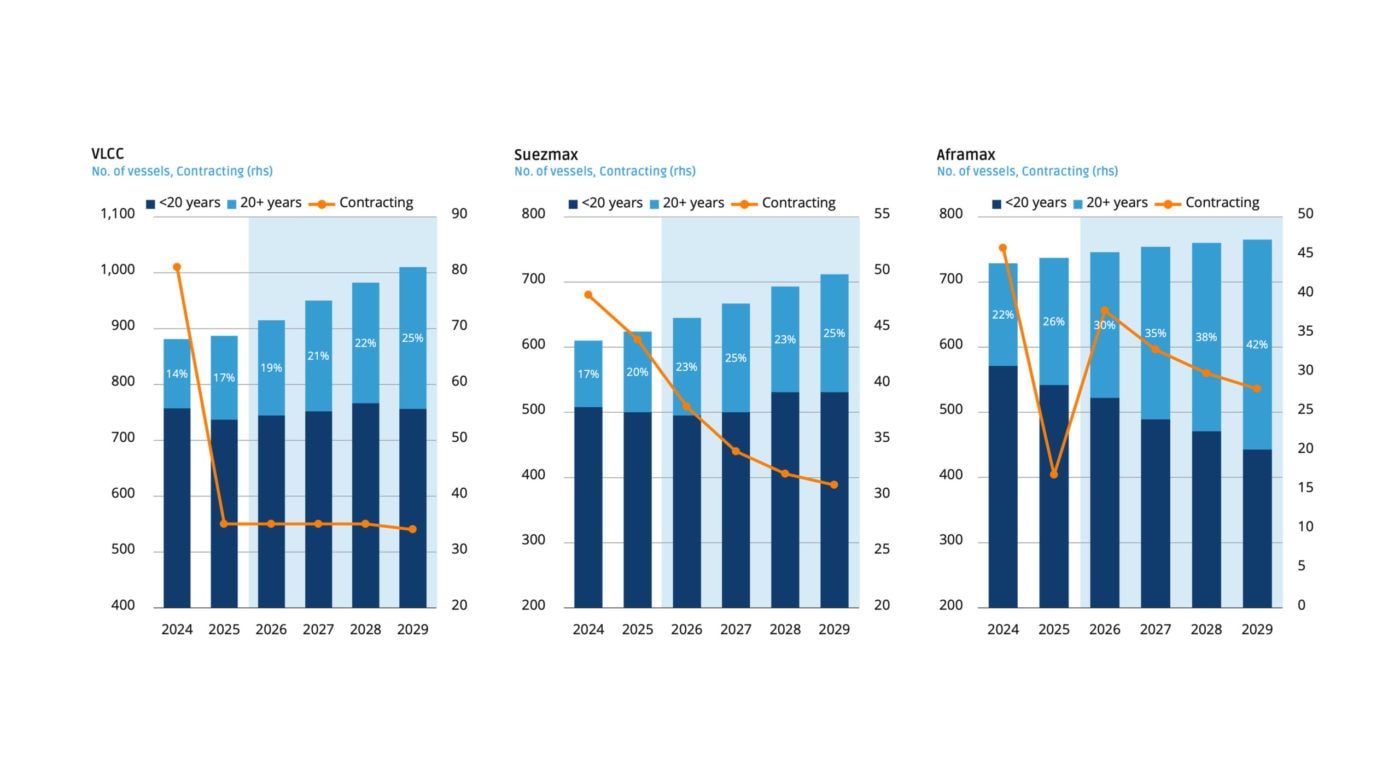

The Crude Segment: A Hidden Tightness

The discrepancy between fleet presence and trading relevance is even more pronounced in the crude segment. Over 55% of Aframaxes, 42% of Suezmaxes, and 39% of VLCCs are now more than 15 years old. Yet their contribution to liftings is far lower than their share of the fleet would suggest. The result: a fleet that looks larger on paper than it truly is in practice.